Transfer out and…

Withdraw cash as and when you need it (Drawdown)

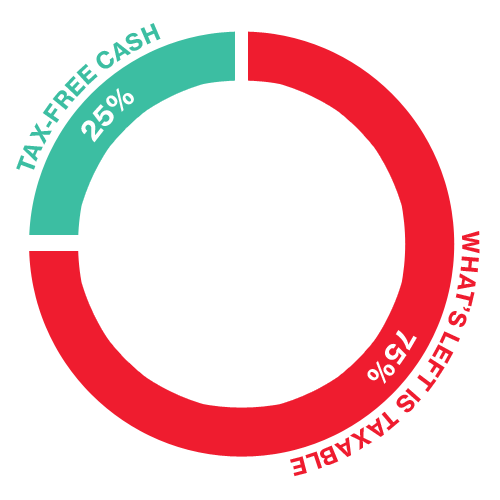

At a glance…

If you choose to transfer out of the Aliaxis DB Scheme and invest your pension savings into a Drawdown fund, you’ll have:

- A fund – where your pension savings remain invested, yet where you can access them when you need to

- Tax-free cash – the option to typically take up to 25% of your transfer value as a tax-free cash lump sum at the point you retire or to take 25% of each withdrawal tax-free

- Withdrawals – the facility to withdraw cash as and when you require it throughout retirement (subject to tax)

- Legacy options – the ability to pass on your Drawdown fund to your dependants when you die.

- the option to buy an annuity at a later date – with whatever savings you have left in your drawdown fund, you can choose to buy a regular income for the rest of your life, called an Annuity

- To take investment risk, pay ongoing investment and potentially advice charges

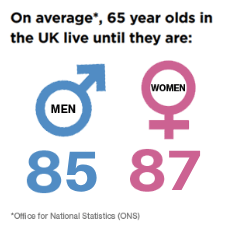

How long might you live?

People are living longer. Improved healthcare, working conditions and a reduction in smoking rates have all contributed to increasing life expectancy from generation to generation.

Understanding how long you might live is an important part of planning for retirement, especially if you’re considering the drawdown option, as you’ll need to make sure your money lasts as long as you need it to.

The National average for a typical 65-year-old, in good health, as at July 2024 is shown on the right.

So, if you are retiring at age 65, you could live for at least 20 years after that (based on data from the Office of National Statistics). That’s 20 years of paying for the things you’ll need and want.

But we’re not all ‘typical’, it’s possible you could live a shorter time or much longer than this. In fact, 1 in 4 65-year-old retiring now could live in to their 90s and 1 in 33 could live to 100, so they’d need to manage their money wisely!

Privani’s choice

Privani wanted flexibility to take her money a bit at a time, changing how much she took and when. After taking financial advice and confirming that this was the right thing to do, she transferred out of the Scheme and took Drawdown.

Privani is used to making investment decisions and knows about the ongoing investment charges. She has a guaranteed income, from other sources to meet her basic needs.

Privani’s choice is just an example and does not suggest a particular option that you should choose yourself. Please look at all of the options available to you and consider seeking independent financial advice before making any decisions about your own benefits.

Why this option might suit you

Here is a list of characteristics that this option provides or doesn’t provide. Have a look through and see if these characteristics suit your personal circumstances. For example, is the reassurance of a regular income for the rest of your life a priority or would you rather withdraw money as and when you need to?

|

The reassurance of a regular income for life | X NO |

Whilst you can withdraw regular amounts this income is not guaranteed to last you for the rest of your life and it’s your responsibility to make it last as long as you need it. You can, however, purchase an annuity at a later date with whatever is left. |

|

Pension increases to protect against inflation | OPTIONAL | You can increase the amount you withdraw to protect yourself against increases in the cost of living (inflation), by this we mean as the cost of things like fuel, bread, milk etc. go up, you can withdraw additional money, but it will run out quicker this way. |

|

A pension for my spouse/civil partner/qualifying dependent on my death | X NO |

You can pass on your drawdown fund to your dependants when you die, but this is not the same as the regular income they could get if you took the Aliaxis Pension or a joint-life annuity. |

|

Leaving an “inheritance” | ✔ YES | You can pass on your drawdown fund to your dependants when you die (typically tax-free if you die before 75). |

|

Something easy to manage | X NO |

Drawdown requires you to manage your investments and your money, to make sure it lasts as long as you need it to. |

|

Money to use now | ✔ YES | You control how much you withdraw and when. You can typically take up to 25% of your transfer value as a tax-free cash lump sum when you retire or 25% of each withdrawal tax-free. See ‘When should you take tax-free cash with drawdown?’ below for more details. |

|

The flexibility to change my income when I like / need | ✔ YES |

You control how much you withdraw and when. |

|

The ability to invest my money myself | ✔ YES |

Any money not yet withdrawn will need to be invested. Your chosen drawdown provider will have various investment options for you to choose from. You should consider the impact of any ongoing investment and advice fees on your fund and the money you can then withdraw. Investments, and any income from them, can go down as well as up and you may be able to withdraw less than you started with. |

|

Suitable if I expect to live a long time | POSSIBLY |

You control how much you withdraw and when, so this depends on how you manage your money, how your investments perform, how much you withdraw each year and how long you live. It’s worth noting that on average (based on national figures from the Office for National Statistics) we’ll live until our mid-80s, however there’s a 1 in 4 chance you’ll live in to your 90s and 3 in every hundred people retiring now will live to be 100 years old. |

Tax

Tax-free cash lump sum

- You can typically take up to 25% of your transfer value or 25% of each withdrawal as a tax-free cash lump sum

- If you die before age 75, you can generally pass your savings to an eligible dependant tax-free.

- The amount payable as tax-free cash is restricted by the Lump Sum Allowance (LSA) and the amount payable to your dependants may be restricted to the Lump sum and death benefit allowance set by the Government (see Tax & State benefits section)

Income (subject to tax)

- Withdrawals above your tax-free cash allowance will be taxed at your marginal rate of income tax for the year in which you make the withdrawal (20%, 40% or 45%)

- You won’t pay tax on investment returns within your Drawdown fund.

- On death after 75, the savings remaining can be drawn down or paid as a lump sum, taxed at your eligible dependant’s marginal rate.

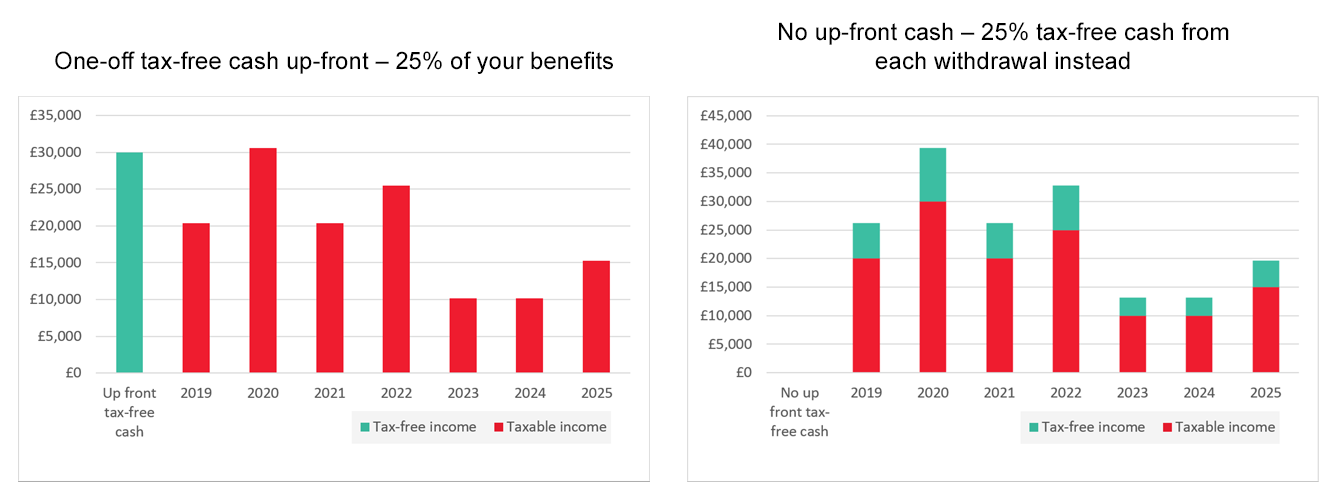

When should you take tax-free cash with drawdown?

When you enter drawdown, you typically have the option to either take 25% of your transfer value up front as a tax-free cash lump sum, or you can take a 25% of each withdrawal you make tax-free (subject to the Lump Sum Allowance – Tax & State benefits section). Whether you choose one way or the other will depend on your personal circumstances and tax position, so it’s worth speaking to a financial adviser for advice.